Authors: Guy Stuart (Microfinance Opportunities) and Sara Litke-Farzaneh (Mathematica)

Data visualization: Gray Collins (Mathematica)

Authors: Guy Stuart (Microfinance Opportunities) and Sara Litke-Farzaneh (Mathematica)

Data visualization: Gray Collins (Mathematica)

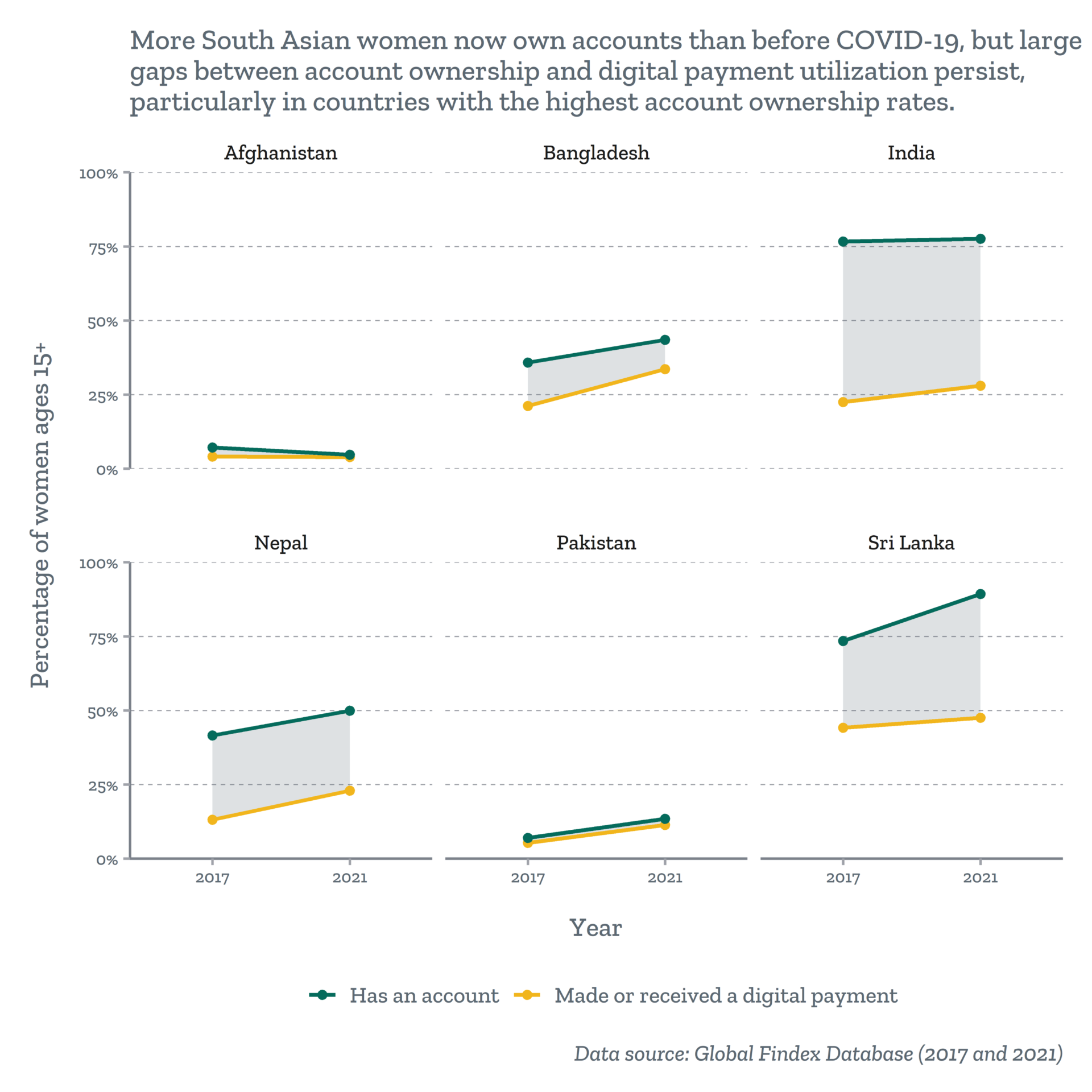

During the COVID-19 pandemic, governments, philanthropic donors, and private companies across the globe deployed emergency payments at a massive scale to provide financial support in the face of an economic shutdown. Most of these payments were made digitally rather than in cash to adhere to social distancing measures. This led to the rapid opening of financial accounts: an unexpected on-ramp to financial inclusion for tens of millions of women in low- and middle-income countries (LMICs). The World Bank’s Findex data show that the share of women in LMICs with financial accounts increased by 10 percentage points (from 59 to 69 percent) between 2017 and 2021, and the share who made or received a digital payment increased by 13 percentage points (from 39 to 52 percent).

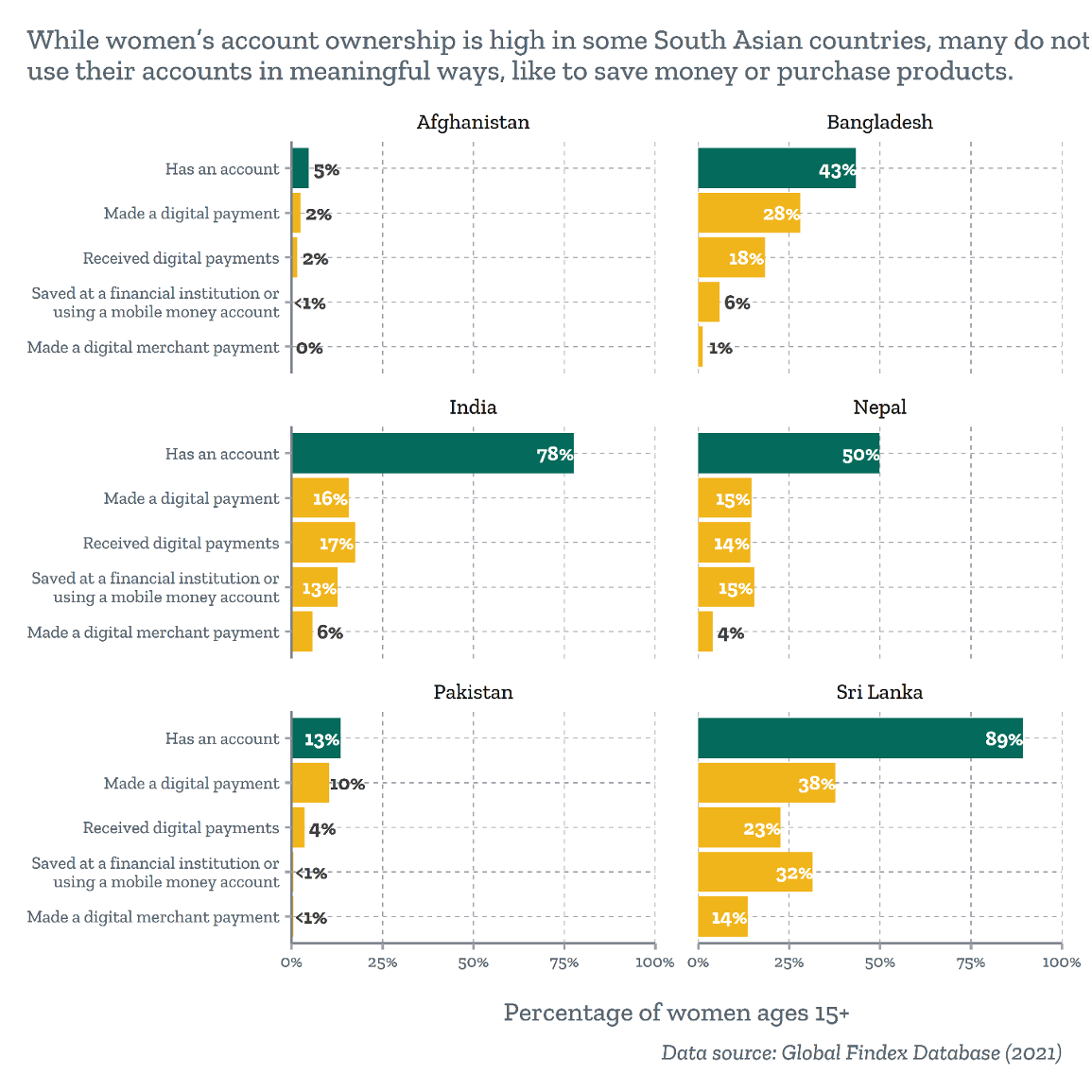

However, many of these women, especially in South Asia, don’t appear to be using their accounts to make or receive a payment (including remittances). In Bangladesh, India, Nepal, and Sri Lanka—which collectively are home to 592 million women—account ownership is now relatively high compared to the past decade, but account usage still lags behind ownership.

New accounts do not immediately or automatically result in account use beyond a few activities. This suggests that more must be done to these recent trends in increased women’s account ownership to fully deliver on the promise of financial inclusion to improve women’s economic empowerment.

A good place to better understand this phenomenon is in Bangladesh, where women’s account ownership increased by 8 percentage points (from 36 percent in 2017 to 44 percent in 2021), according to Findex data. A big driver of this increase was the government’s active promotion of financial inclusion during the early part of the COVID-19 emergency through a variety of initiatives, including a digital wage payment support program for workers in the apparel export sector who were furloughed during the lockdown. This program resulted in 1.2 million women opening digital bank or mobile money accounts within a single month—demonstrating that digital wage payments can enable access to critical funds during an emergency and generating trust in the digital financial system. Women’s account usage also increased during this timeframe: while 17 percent of women account holders made or received a digital payment in 2017, 28 percent did so in 2021. In theory, this rapid wage digitization could have led to significant welfare randomized controlled trial led by the World Bank in 2020 showed that wage digitization for factory workers in Bangladesh led to greater savings, control over income, and ability to cope with unanticipated economic shocks.

To understand whether wage digitization had this same effect on women factory workers in Bangladesh in the large-scale, real-world policy setting of the COVID-19 government stimulus package, Mathematica partnered with Microfinance Opportunities (MFO) on a study funded by the Bill & Melinda Gates Foundation. Using MFO’s rich garment worker diary data set and interviews with workers, factory management, financial service providers, and other public and private sector actors, we learned that this rapid wage digitization led to a massive increase in women’s account ownership and a significant gain in women’s financial inclusion, but that women still face barriers in fully using their accounts. We found that the share of women garment factory workers receiving their wages digitally went from 28 percent before the pandemic to a peak of 76 percent during the wage support program, eventually declining to a steady state of 54 percent after the program ended. The stimulus package successfully lifted many barriers to wage digitization by eliminating account opening fees, subsidizing cash-out fees, and relaxing requirements for identification documentation to open accounts. Together, these led to a rapid increase in women’s account ownership that allowed women garment workers to receive their wages during a time of crisis.

|

“When my salary comes as digital payments, I have control over my money. It can be spent [only] as much as needed. By reducing the cost in this way, money can be saved.” |

Our data reinforce the existing evidence (such as in Allen et al. 2022) that wage digitization is a driver of digital payment acceptance. When MFO interviewed women workers after the lockdown, in September 2020, 65 percent said they were comfortable the system of digital payments. Later, in 2021, 61 percent of workers said they trusted their factory management more if they paid digitally. By 2022, workers were more likely to cite advantages rather than disadvantages of receiving digital wages. These included the timeliness and safety of digital payments, the ease of transactions, and the ability to save.

Nonetheless, 52 percent of workers who were paid digitally after the stimulus (and 75 percent of workers who were paid in cash) reported preferring cash. When we dug deeper, it became apparent that this is due to the context of a cash-based economy: women workers said they couldn’t use their digital accounts in many meaningful ways, like to pay merchants, rent, or school fees. The most prominent use case was sending remittances to families (39 percent of workers). Twenty-nine percent of workers said they just cashed out their wages, which had a cost both in time and in a withdrawal fee. Twenty-nine percent of workers also said they didn’t know how to use their accounts for other purposes, and 19 percent were dependent on their husbands or other family members to use their accounts. Only 14 percent used their accounts to save after the stimulus.

A closer look at our data shows that one reason for this low use of digital accounts was that women workers didn’t receive the training they needed to use their account effectively. Seventy-eight percent said they only received basic support or information, rather than trainings, from their factory on opening and using accounts, and only 17 percent said they were aware of the types of transactions they could make.

Another key reason for low use of digital accounts appears to be the reluctance of the private sector– both factory employers (mid-level management), and the businesses where garment workers tend to spend their money (for example, retail micromerchants, schools, pharmacies, and landlords and their agents). , many factory managers we interviewed did not see the benefits of wage digitization or did not feel they outweighed the costs, particularly of covering cash-out fees (after the stimulus program ended, cash-out fees re-emerged as a key barrier). Some interviewees thought private sector actors were concerned about the transparency of digital payments: merchants, because they would have to pay license fees or taxes; and factories, because paying wages digitally exposes possible fraud or leakages in pay. Some of this reluctance around digital pay is also likely due to commensurate weaknesses in the enabling environment provided or supported by other stakeholders such as the government, civil society, and multinational corporations sourcing goods in Bangladesh.

Our findings from Bangladesh provide insights into ways to leverage these trends in increased digital account ownership toward an ecosystem that offers women more choice and value from their accounts.

Promote the acceptance of digital payments by small and micromerchants.

Garment workers often shop at small, informal shops, most of which do not yet accept digital payments. The World Bank studied the factors that were most closely associated with small and micromerchants’ acceptance of digital payments. This included a general prevalence of accounts in the economy, which means promoting account ownership is critical and should be coupled with support for a robust digital finance infrastructure (which was demonstrated in Bangladesh during the pandemic). However, there is still work to be done in Bangladesh, including on whether the merchants themselves pay their suppliers and employees digitally, and, as some of our interviewees indicated, on the role that taxes play in deterring merchants from accepting digital payments. To incentivize micromerchants to accept digital payments, Bangladesh Bank has provided bonuses and created new retail accounts that can be opened with minimal requirements, including national IDs and a certificate of proof of profession. They are also exploring loan or credit facilities with micromerchant accounts, as well as partnerships with international agencies to cover payment fees.

Continue to make the case for the benefits of wage digitization and the costs of cash.

The Government of Bangladesh, international brands, and public and global advocacy organizations like the BTCA should continue to push for wage digitization and fulfill commitments made at the 2019 Digital Wages Summit. A new toolkit from Reimagining Industry to Support Equality can also help mid-level factory managers understand how to digitize wages and why it’s worthwhile from a business perspective.

Identify strategic initiatives to promote women’s use of digital payments.

Women with digital accounts need better access to information and quality training about how to manage their account securely, store savings, and take advantage of existing digital payment opportunities like mobile top-ups and bill payments. This is a priority in the new and will prepare women to be willing and able users of digital financial services as new opportunities arise. Banks and other financial service providers profit most when money is used digitally, so they have a financial incentive to provide these trainings (in collaboration with factories, and ideally with trusted local community and peer networks) to ensure that women are ready to use their accounts.

In addition, as the government, financial institutions, and Fseek to build up the digital payments ecosystem, they should target those parts of the system that women are most likely to interact with and integrate digital and financial capability-building elements into their products (designed based on women’s needs and experiences). For example, women are often the ones who pay children’s school fees and basic household expenses such as food. Digital financial providers could offer a loan product that allows women to pay school dues in installments if they are transferred digitally. Allowing women workers to pay for food on credit through digital financial providers could also be beneficial for both women workers and merchants; digital payments would create transaction transparency for merchants, while increasing workers’ resilience and choice in household expenditures.

Cover cash-out fees while the digital ecosystem is being built up to prevent losing account-holders.

One important lesson from the Bangladesh experience is that people prefer receiving cash wages over digital if they cannot make digital payments themselves and have to pay fees to cash out. One way of making digital wages more acceptable in the short run, while the digital ecosystem is being built up, is to ensure that workers don’t pay large cash-out fees. For example, both the Reserve Bank of India and mobile financial service provider (MFSP) SadaPay in Pakistan allow for three free cash withdrawals per month. Alternatively, the government could follow the ILO’s recommendation of mandating that employers pay full wages digitally, which would include cash-out fees. Bangladesh could take one of these approaches to minimizing or covering cash-out fees, not because it will increase digital payments, but because it will reduce reluctance around digital pay. Similarly, strengthening the digital ecosystem to be interoperable would also support women’s engagement in the digital economy by expanding access and availability of agent and ATM options, and eliminating extra fees by allowing women to send money directly from their account with one MFSP to a relatives’ account with a different MFSP.

In sum, digital wages can serve as an unprecedented on-ramp to financial inclusion for women workers, as they have in Bangladesh. However, for women to take full advantage of their accounts, they need to be able to engage with a functioning digital money ecosystem that includes products designed for women and access to sufficient training on how to use their accounts. Resolving these issues is a critical step to more fully deliver the promise of financial inclusion for women’s economic empowerment.